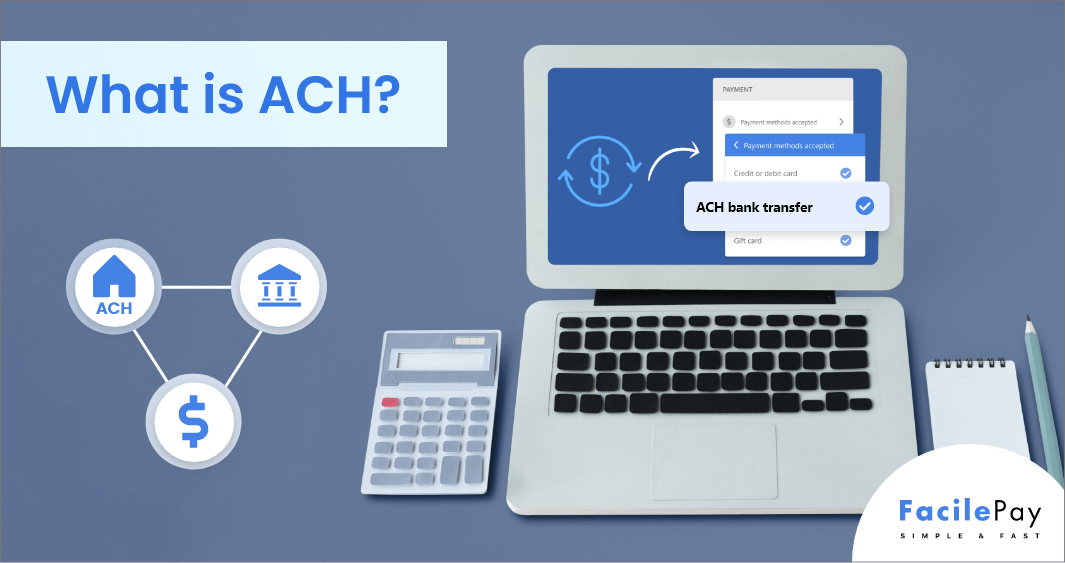

- Automated Clearing House (ACH) payments are electronic transfers of funds between bank accounts in the US.

- ACH payments are secure, reliable, and cost-effective compared to other payment methods.

- ACH payments can take 1-3 business days to process, so plan accordingly.

- ACH payments can be used for various purposes, including payroll, vendor payments, and recurring billing.

📝Key Takeaways:

Next to cash, debit, and credit cards have become popular to process any payments. If credit and debit cards are in demand, then why do businesses want to explore other mediums of electronic payment?

The simple answer to this is the high debit and credit card processing fees associated with each transaction. This is when the automated clearing house (ACH) payment system, popularly known as one of the electronic transactions, comes in.

According to NACHA, there’s steady growth for the ACH network by 2022 with 7.6 billion payments valued at $ 19.2 trillion.

To understand how ACH payments work, you need to read this blog further.

-

In the next 10mins, you will learn:

- What is ACH, and how does ACH work?

- Why should businesses use ACH?

- Benefits and limitations of using ACH payments

Let’s get started.

Contents

What is an Automated Clearing House (ACH)?

ACH is an electronic funds transfer system that shares similarities with paper-based checks. The primary difference is that ACH is a digitized payment often referred to as

- Electronic fund transfers

- eChecks

-

Key Takeaways

- The ACH network is regulated by one of the federal reserve banks- NACHA.

- To make the payments on the same business day, the ACH rule has changed to ACH debit transfers and ACH credit transfers.

- ACH transactions make payment services easy and quick.

Let us now understand how ACH transactions work for businesses.

How Does Automated Clearing House Work?

- Paying a bill online from your bank account.

- A direct deposit from an employer as a paycheck.

- Transferring funds from one bank account to another.

You might have got a blurred vision of how ACH works from the above examples. To be clear, the working of ACH transactions works with forwarding and receiving funds from an originating depository financial institution and a receiving depository financial institution.

The rotation goes around like this:

- Originator starts direct deposit or payment using the ACH network

- ODFI collects files and sends a batch to ACH

- ACH operator batches transactions together with other ACH transactions

- RDFI pulls funds from the bank and sorts the batch to make transactions

- The recipient bank receives the funds and the process ends here

With the above working of ACH payments, you might now want to know how it benefits your business. There are a few reasons why businesses should use direct deposits.

Let’s discuss.

Key Reasons to Integrate ACH Transfers for SaaS Business

Automated clearing houses can serve as a great option for SaaS businesses. SaaS platforms that provide recurring billing know that collecting payments is the top priority of business.

The biggest concern today in any business is the massive increase in credit card declines. Some of the statistics say that on average 15% of recurring credit card payments decline.

Thus, offering ACH transactions are safer and become mandatory for recurring payments. There are indeed two major reasons why you must opt for integrating the ACH payment option.

Reason #1: ACH payment decline rates are less than credit cards. Depending on the industry SaaS ACH network decline rates are less than 2% compared to 15%.

Reason #2: ACH direct deposits have reduced payment fees. For example, for a $100 average sale with credit cards, you can expect $2.50+ in processing fees. For an ACH transaction, there is a flat 30 cents processing fee.

Other reasons why SaaS businesses should choose an ACH operator for electronic funds transfer are as follows:

- Recurring payments: ACH payments are ideal for recurring payments, especially for SaaS businesses. ACH allows direct deposit to the account, eliminating the need for manual invoicing and payment.

- Security: ACH direct payments are secured by NACHA rules and regulations. This can help to reduce the risk of fraud.

- Widely accepted: ACH transfers are widely accepted by small businesses and consumers as this makes it convenient and flexible for them.

- Integration: ACH electronic payments network can be integrated with the businesses existing billing systems, making the payment process seamless.

Given the above reasons, you can collect more revenue and leverage that in your client acquisition strategy. With every digital payment network, there comes a few disadvantages. Let us now understand the pros and cons of using an automated clearing house network.

Pros and Cons of Using ACH Payments for Business Accounts

Transferring money or receiving money from your customers is always a worry. No business wants its money to go missing.

ACH payments come with the safest and most secure way for bill payments. However, let us study a few advantages and limitations of these ACH payments.

- Easiest and low-cost ACH payment transfer between US bank accounts.

- Using ACH payments is much safer than any wire transfer, as you can reverse debit transactions.

- Setting up recurring transfers can avoid missing payments or delayed consumer bills.

- Lower transaction costs than other financial institutions like wire transfers via credit or debit cards.

- Higher retention rate as banking transactions are safer than cards.

- Transfers can take up to 4-5 working days.

- Limited overseas use for international businesses.

- ACH payment is not ideal for high-volume, and critical or urgent payments.

- ACH transfer limit is capped at around $25,000, which may be too low for some businesses.

From sending and receiving payments from consumers, many transfer providers are available. But, with the ACH network, it is easy for any electronic transaction. Given in the next section, we discuss the types of ACH transfers.

2 Types of ACH Transfer

There are typically two types of direct deposit ACH transfers.

1. ACH Credits

This type of transfer is used to deposit funds into the recipient’s account through originating depository financial institutions. For example, direct deposit of payroll, automatic bill payments, and electric tax payments.

2. ACH Debits

This type of transfer is used to withdraw funds from the customer’s account. The payments are released from receiving depository financial institutions and sent to the merchant’s bank account. For example, automatic mortgage payments, recurring monthly subscriptions, and one-time payments for products or services.

Most ACH payments are processed through the ACH network which is considered a secure and reliable system in the USA.

So when is it feasible to use ACH payments in any business? Let’s dig into the details.

When to Use ACH Payments?

ACH payments are typically used in situations where businesses need to make or receive electronic payments on a regular basis. Some examples of when to use ACH payments include

-

Recurring Payments

ACH payments can be set up for recurring payments, making it easy for businesses to collect payments from customers on a regular basis, such as monthly subscriptions, and rental payments.

-

Direct Deposit

For direct deposit of payroll, ACH payments should be used that allow employees to receive their wages electronically, rather than via a paper check.

-

Automatic Bill Payments

Use automatic bill payments to automatically pay bills, such as mortgages, car loans, and utility bills.

-

Electronic Tax Refunds

ACH payments can be used to receive electronic tax refunds, which can be faster and more secure than receiving a paper check.

-

High-volume, Low-value Transactions

ACH payments can be a cost-effective option for businesses that need to process a high volume of low-value transactions, such as micropayments.

-

B2B Payments

Make payments to vendors and suppliers, which can be faster and more secure than writing a check with direct banking transactions like automated clearing houses.

It is worth noting that ACH payments are typically used within the United States, so they may not be an option for businesses that need to make or receive payments from foreign countries.

If you have more questions on ACH, we have curated a list of frequently asked questions for you.

Frequently Asked Questions

-

How do ACH payments work?

ACH payments work by pushing funds digitally between bank accounts. The sender initiates the ACH transfer by providing the bank account information with the recipient’s account, including the routing number and checking account number. The funds are then sent to the recipient’s savings account.

-

Can ACH payments be reversed?

Yes, ACH payments can be reversed. This process is called an ACH return. ACH returns can be initiated by the receiving bank, the originating bank, or the account holder of the authorized entity. There are specific timeframes and reasons for which an ACH payment can be returned. Some common reasons include insufficient funds, a closed account, invalid account numbers, and unauthorized transactions.

-

What is the difference between an ACH Debit and an ACH Credit payment?

An ACH debit is a transaction where funds are transferred from one bank account to another, and the account holder authorizes the transaction.

On the other hand, an ACH credit is a transaction where funds are transferred from one bank account to another, and the payee initiates the transaction.

-

How long does it take for an ACH payment to clear?

An ACH payment typically takes 4-5 business days to clear. However, it can take longer depending on the financial institution and the time of day the payment was initiated.

Make the Switch from Paper Checks to Automated Clearing Houses (ACH)

So what do you think- are ACH transactions good for your business?

Or do you still want to continue with paper checks?

It’s time to stop the paper checks. Clearing houses are easy to use where you can save money and apply these savings to other important aspects of the business.

ACH opens doors for quick payment systems and builds a bridge to complete financial transactions in just a couple of business days. Maximize profitability and elevate the customer experience from a single platform.